To achieve savings benefits from the coming wave of biosimilars, biosimilars must be adopted by prescribers, members, and payers (through their formulary strategies). While previous biosimilar launches have produced some initial savings by driving down the price of the reference product without realizing significant biosimilar utilization, the most competitive biosimilar markets have robust biosimilar utilization. Without this three-fold adoption, the utilization of biosimilars will be suboptimal, and therefore the realized savings from biosimilars will also be suboptimal.

- Prescriber Adoption – prescribe biosimilars to new patients and move existing patients to biosimilars

- Member Adoption – address concern about efficacy/safety, encourage members to seek out biosimilars

- Formulary Design – various strategies to steer usage towards biosimilars with formulary design

What does it take for prescribers to be comfortable prescribing biosimilars? First, they must have familiarity with the biosimilars.

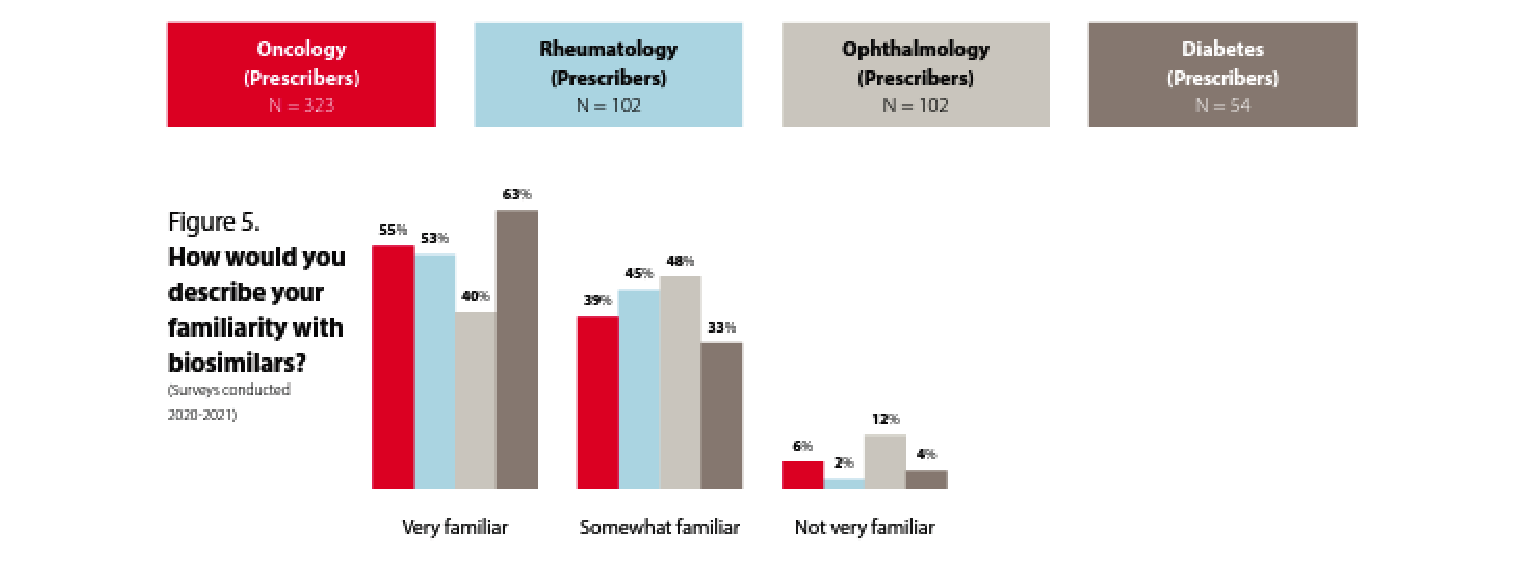

Prescriber familiarity with biosimilars differs by specialty

Prescribers seem to be familiar with biosimilars. While the level of familiarity varies somewhat by specialty, across all these specialties around 90% or more of the prescribers are either very familiar or somewhat familiar with biosimilars.

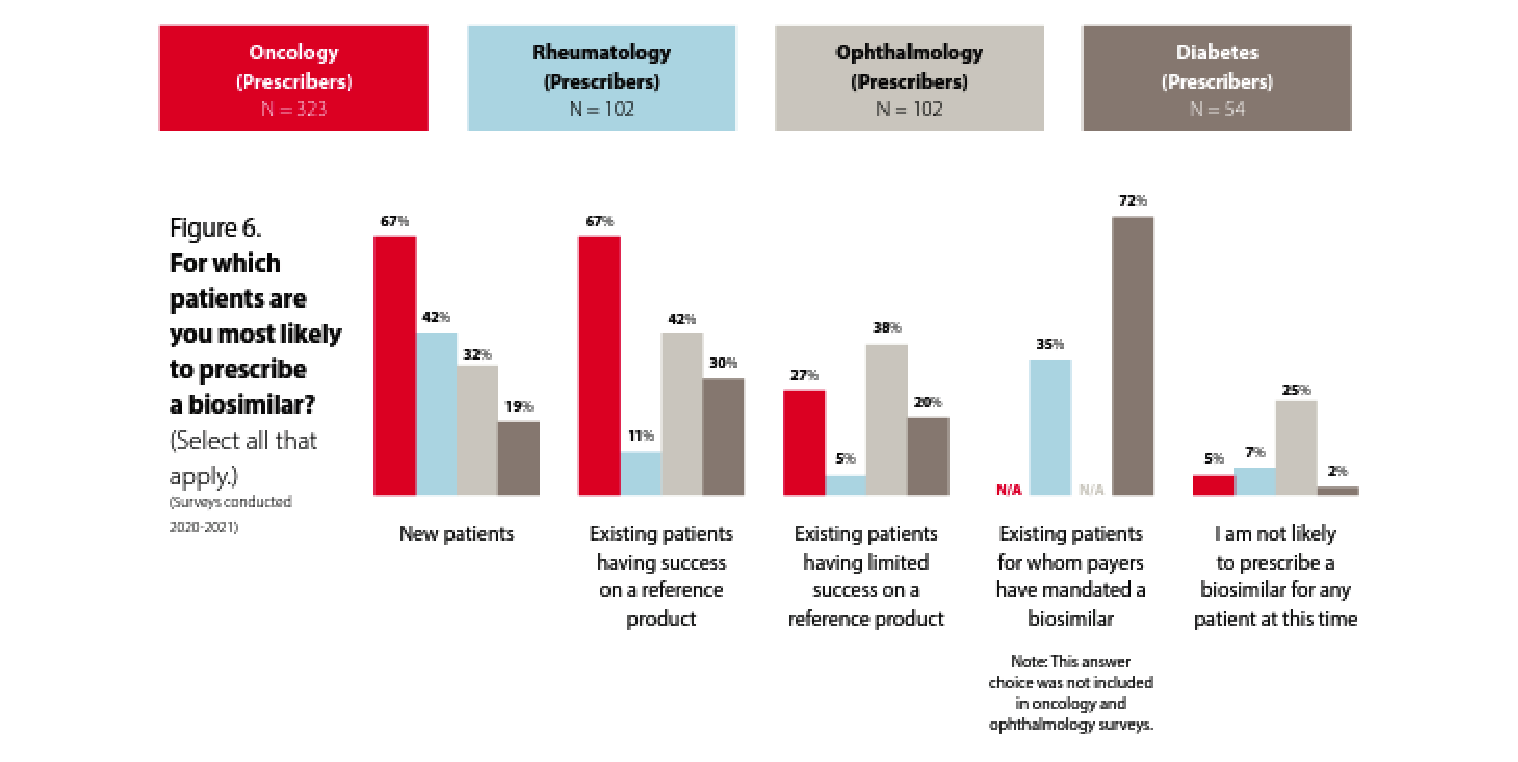

But what about their prescribing patterns?

The majority of participating physicians are familiar with biosimilars, but prescribing patterns vary by specialty.

In oncology, we see a greater likelihood to prescribe biosimilars for new patients and existing patients who are having success with a reference product. Only 27% of oncologists are likely to prescribe a biosimilar for patients who are having limited success with a reference product. These data points seem consistent and are presumably because the oncologists recognize the biosimilar as acting therapeutically similar to the reference product. Some have suggested that oncologists are more familiar with rapid innovation because of the historically rapid development of new chemotherapy products. In addition, oncology pharmacy purchasing decisions may be made by a facility’s formulary review board as opposed to in an office setting between a patient and provider, and oncology patient panels can turn over rapidly due to the nature of the disease being treated.

The familiarity with and willingness to prescribe biosimilars in rheumatology, ophthalmology, and diabetes seems to be lower. That said, 72% of prescribers are likely to prescribe a biosimilar to treat diabetes if it is mandated by the payer, which shows a possible path toward accelerating biosimilar uptake. Of course, payer mandates are not always viewed favorably by patients and prescribers and need to be thoroughly considered from the clinical and patient disruption perspectives before being applied.

Rheumatologists are much less likely to prescribe biosimilars for existing patients who are having success with a reference product than they are to prescribe a biosimilar to new patients. Does this represent the hesitance to “change what’s working” for rheumatology patients? Let’s dig a little deeper into rheumatologists’ perspectives on biosimilars.

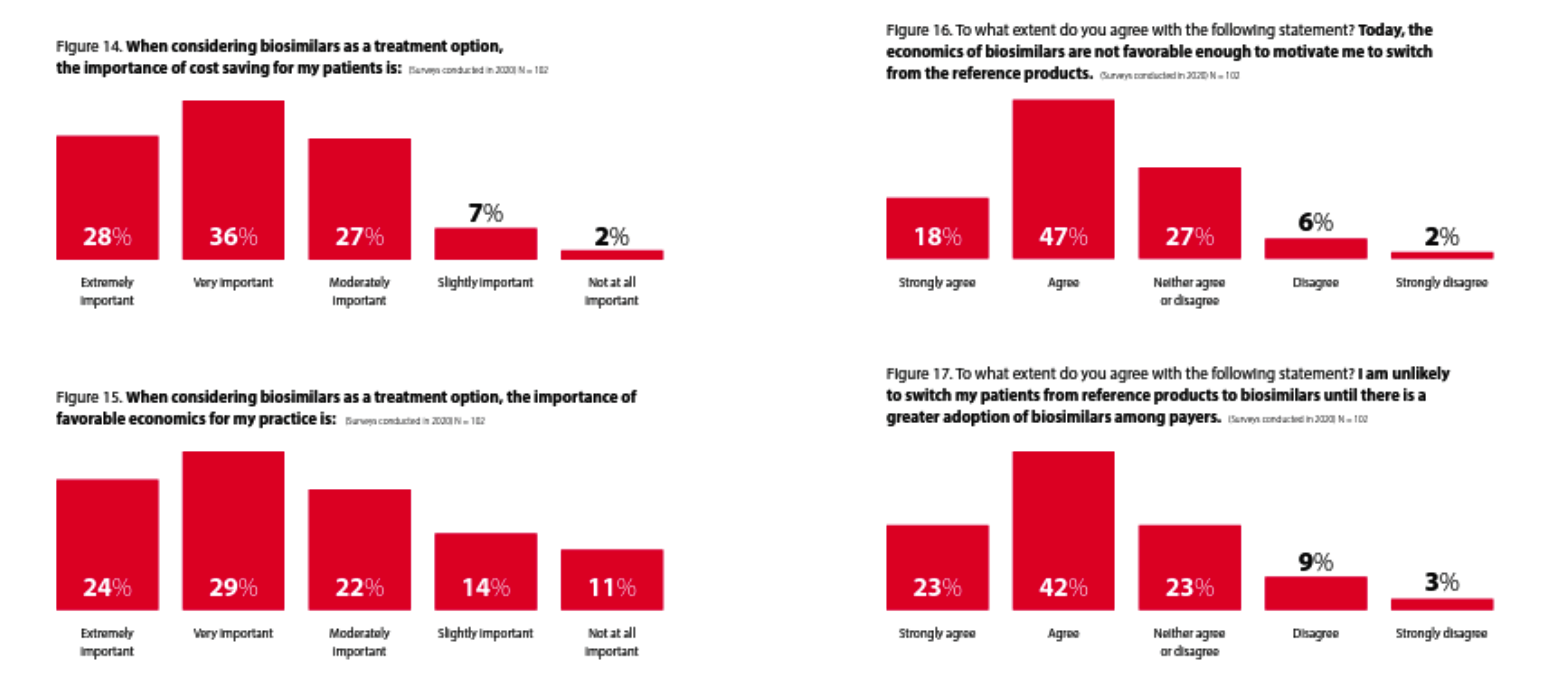

Rheumatologists view cost savings to patients as important, though agree “the economics of biosimilars are not favorable enough to motivate me to switch”

This survey shows that while rheumatologists think the economics are important, they do not think the economics of biosimilars are favorable enough yet (in 2022) to motivate them to “switch from the reference products.” It will be interesting to see if that changes as we enter the back half of 2023 and many more Humira biosimilars become available and that increase in competition presumably drives net prices down.

Whether that occurs primarily through rebates (where the economic impact on patients is less but can produce significant revenue for providers who are 340B qualified entities) or through significant declines in list prices (where patients are more likely to benefit significantly) could make a big difference. Whether or not Humira prices follow could also make a big difference in whether or not rheumatology prescribers feel the economics of biosimilars change enough to motivate a “switch from the reference products.”

It is also not clear whether “the economics” is referring to the economics for the patient or the economics for the prescriber. If payers want to motivate biosimilar uptake they are also going to have to consider prescriber economics and how to ensure they are aligned with the rest of their biosimilar strategy.

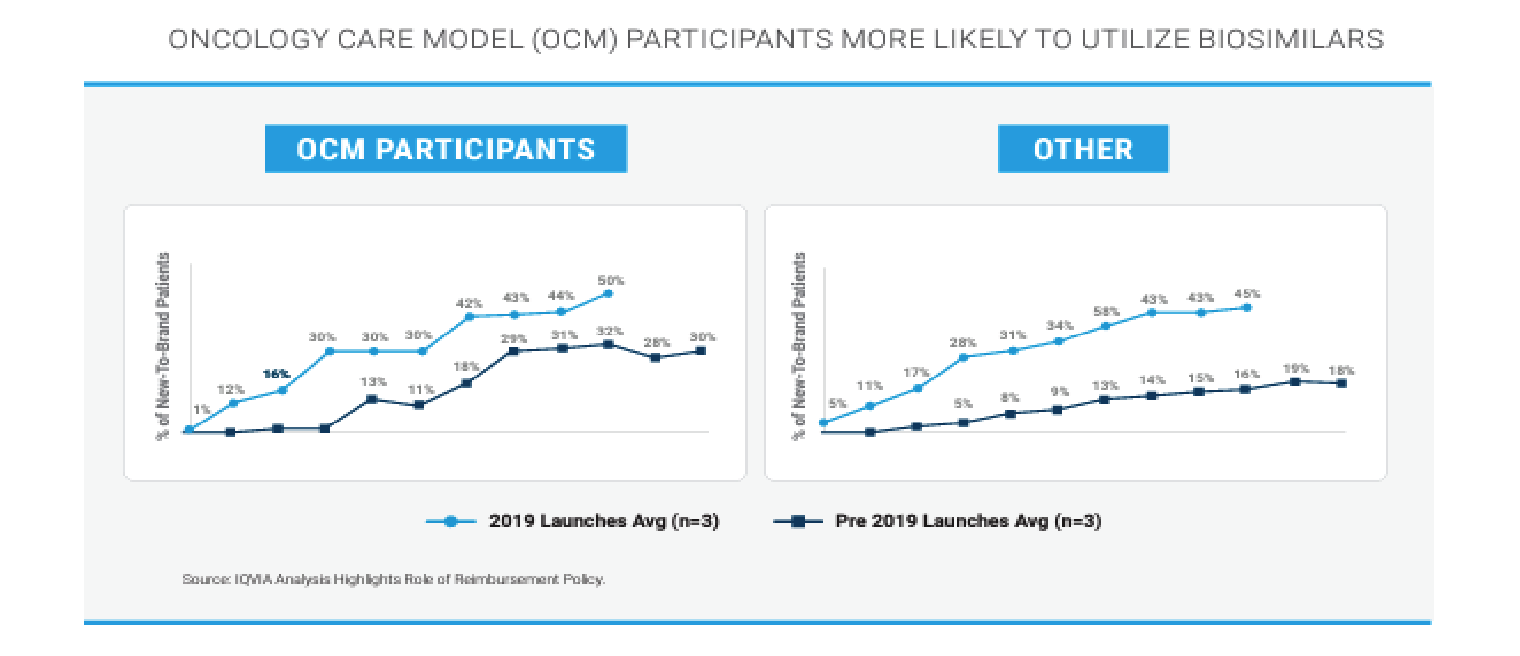

Provider Financial Incentives and Education can Drive Biosimilar Adoption

Based on this analysis of the use of biosimilars inside and outside of CMS’ Oncology Care Model (OCM), it appears that financial incentives for oncologists do increase their likelihood of prescribing biosimilars.

Inflation Reduction Act Biosimilar Add-On Payment

Medicare Part B drugs (administered and paid through the medical benefit instead of through the pharmacy benefit) are reimbursed at 106% of the average sales price (ASP). The 6% “add-on” payment is meant to cover providers’ acquisition, storage, and dispensing costs. Under the Inflation Reduction Act (IRA), biosimilars will be reimbursed at 108% of the reference drug’s ASP.

This increases the current reimbursement for biosimilars administered and paid through Medicare Part B by at least an additional 2%. But also by the additional margin amount if the providers can obtain the biosimilars at a lower cost than they can obtain the reference biologic. The IRA is creating a financial incentive for providers to prescribe and administer biosimilars since the margin for providers who administer biosimilars would be at least 2% more than it would be if the providers administered the reference biologic.

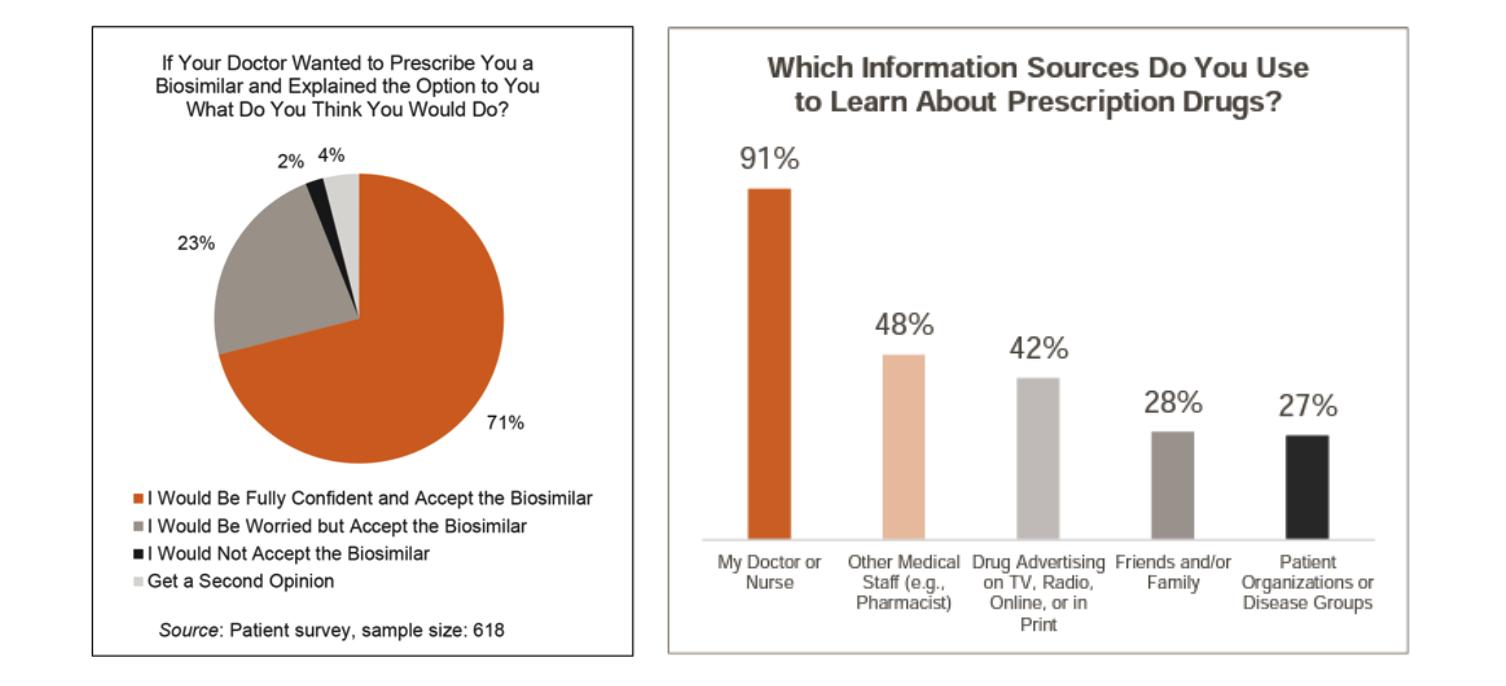

Patients Look to Their Doctor for Guidance on Moving to a Biosimilar

According to this survey, patients are highly likely to follow their doctor’s recommendations regarding the prescribing of biosimilars. 94% of patients would switch to a biosimilar even if they are “worried” about it (23% of patients).

Source: https://www.norc.org/PDFs/Biosimilars/20210405_AV%20-%20NORC%20Biosimilars%20Final%20Report.pdf

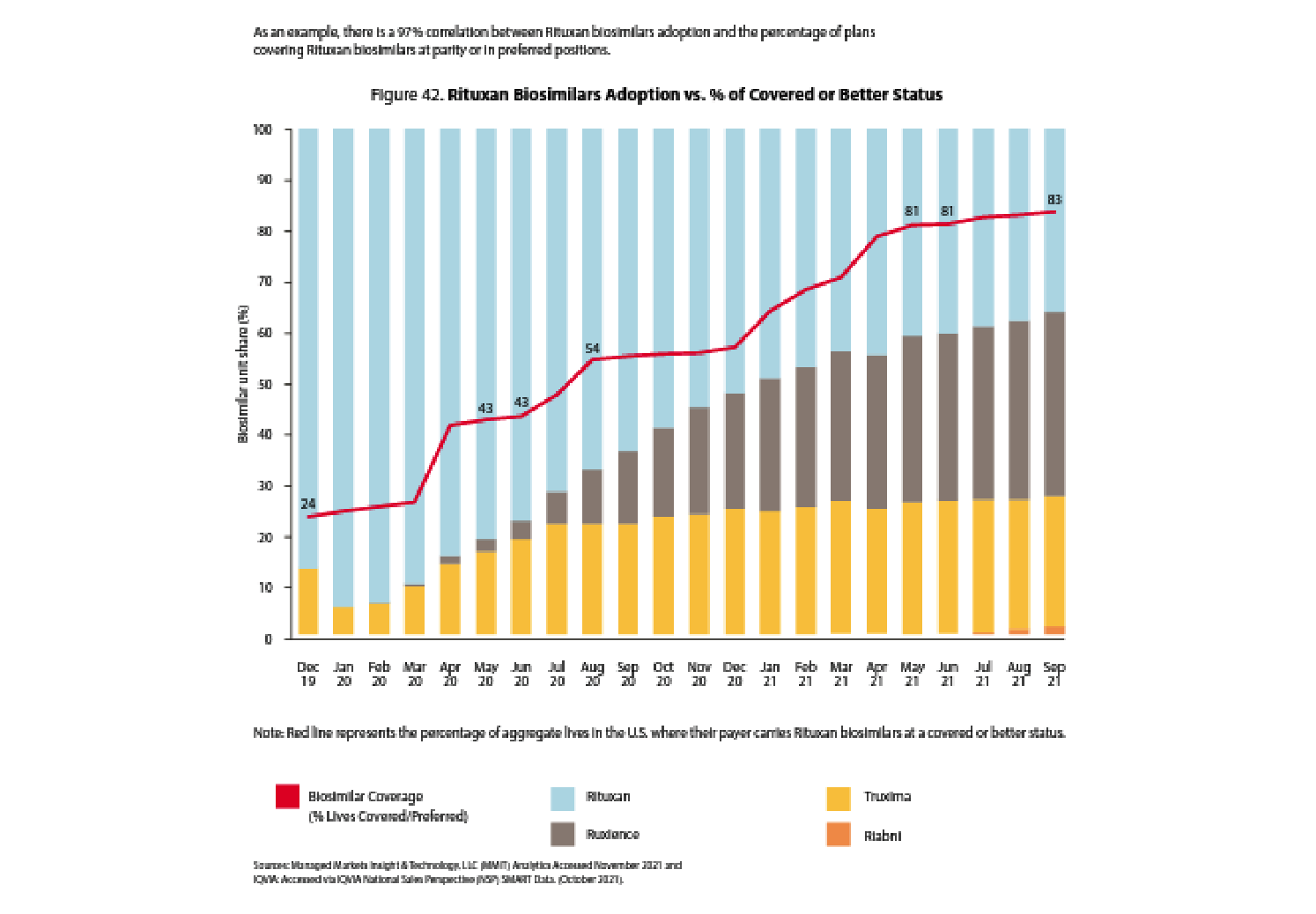

Payer Formulary Coverage of Biosimilars is a Precursor to Prescriber Adoption

Even if prescribers and patients are motivated and incentivized to utilize biosimilars, the payer has to enable that by placing the biosimilars at parity or in preferred positions to the reference drug on their formularies.

“Even if prescribers and patients are motivated and incentivized to utilize biosimilars, the payer has to enable that by placing the biosimilars at parity or in preferred positions to the reference drug on their formularies.”

It is uncanny how correlated the red line (percent of plans placing a biosimilar at parity or preferred to a reference drug) is to biosimilar adoption and the related decline in reference drug market share.

Payers have several tools they use to drive biosimilar adoption:

- Indication-Based Formulary: manage formulary strategy for each of Humira’s indications

- Step Therapy: require members to “step through” other drugs before providing preferred coverage

- Preferred/Non-Preferred Tiers: cover reference product on a non-preferred tier that is still “covered” on the formulary but with less advantaged cost-sharing than the preferred tier

Indication-based formularies have not been highly prevalent, but with Humira being approved in nine indications, more indication-based formularies may emerge. You may see other biologic drugs preferred in different indications where there is more competition while still seeing Humira preferred where it is needed for a more unique indication.

Summary

The second half of 2023 will be fascinating to watch. Biosimilar uptake is the key to whether or not savings materialize for payers and patients. Ultimately, prescribers will become more familiar with the Humira biosimilars as many more of them launch in the summer of 2023. Whether patients receive a lot of financial savings from the Humira biosimilars will depend more on whether the biosimilars come to market with higher-WAC and higher rebates (more to the benefit of payers and PBMs and non-utilizing members) or with a lower-WAC and lower-rebate pricing strategy (more likely to drive declines in patient cost sharing amounts). Payer formulary and clinical program strategies will drive utilization.

Will they drive biosimilar uptake? Time will tell.

About the Author

About the Author

Any views or opinions presented in this article are solely those of the author and do not necessarily represent those of the company. AHP accepts no liability for the content of this article, or for the consequences of any actions taken on the basis of the information provided unless that information is subsequently confirmed in writing.