Any views or opinions presented in this article are solely those of the author and do not necessarily represent those of the company. AHP accepts no liability for the content of this article, or for the consequences of any actions taken on the basis of the information provided unless that information is subsequently confirmed in writing.

Introduction

In a traditional economic business model, the tension and interaction between supply and demand in a competitive environment usually leads to rational pricing and reasonable pricing/profit margins. Today’s US health care system varies from the traditional economic business model and faces some unique challenges.

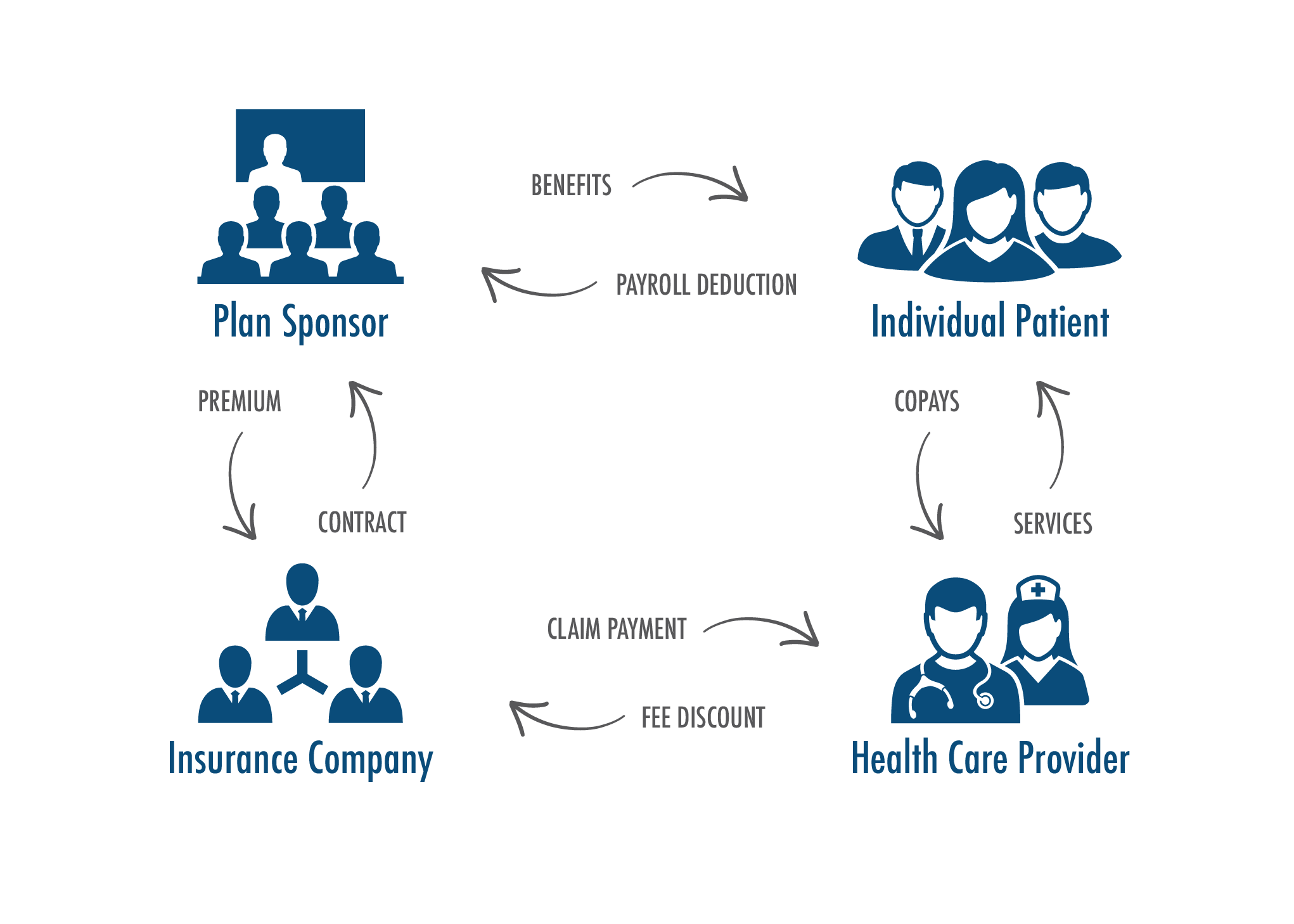

For most beneficiaries, the US health care system has four major stakeholders: individual patient, plan sponsor (i.e., employer or government), the insurance company, and the health care provider. The chart below visually shows this and the various relationships.

The individual patient is what might be called the customer, however, their customer relationship is filtered through multiple stakeholders:

- In the case of work-based insurance and government sponsored programs (i.e., Medicare and Medicaid), much of the health care cost is subsidized by their employer or plan sponsor

- There is limited transparency of the actual provider cost to the individual or patient

- The impact of the provider’s financial and pricing decisions are filtered and diluted through their relationship with the insurance company and the insurance company’s relationship with the plan sponsor, and the plan sponsor’s relationship with the individual.

- To the extent that individual decisions regarding healthcare choices are required, the individual makes these on very limited, diluted and incomplete information.

This article will discuss one aspect of this complex set of relationships, the pricing of hospital and health system services. This article will discuss hospital/health systems accountability as it relates to the pricing of their services. As with other articles, the accountability will be evaluated in terms of Triple AIM, the AHP Accountability Index, and the Accountability Ladder.

Charge-Master Basics

Hospitals and health systems utilize charge-masters to bill their patients for services provided by them. The charge for each service is identified by charge-master code. Services provided to the patient are recorded in the patient’s chart with the total bill for that patient based upon each of these services. In today’s world of electronic medical records, technology is used to capture this inventory of services and related charges, including the submission of this to the insurance company for payment (i.e., using the UB-04 and Form 1500).

The charge-master provides “gross charges” for each service. Payers negotiate discounts with individual providers which results in “net charges” (or what becomes net revenues). The difference between gross charges and net charges (i.e., the discount) is often called the “contractual” or “contractual adjustment”.

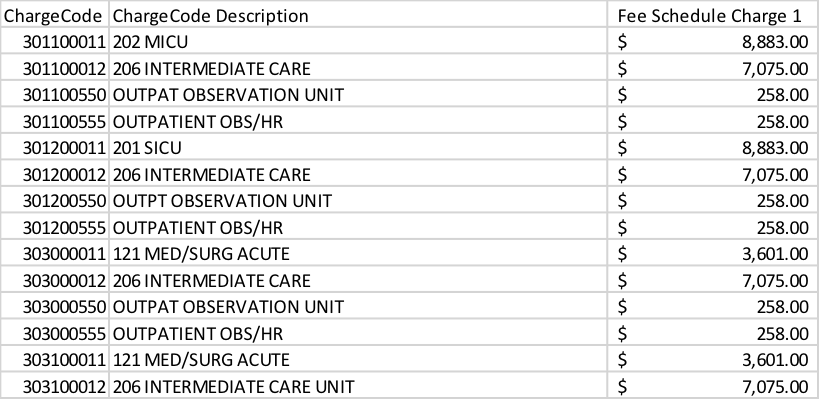

The charge-master is a list of thousands of individual charges. For example, an individual hospital might have more than 25,000 items on their charge-master. Each hospital or health system builds their charge-master to meet their unique needs. There is no consistency between different hospitals unless they are part of a group of hospitals using common practices. The following is an extract of an actual charge-master from California’s OSHPD Charge-master database1.

In addition to the hospital services as shown in the above table, the charge-master will also include charges for supplies, pharmaceuticals and perhaps even professional charges for facility based providers. These latter items are usually based upon a combination of the actual acquisition cost and a mark-up assumption (e.g., $100 x (3.0) for a mark-up of 200%). The service portion of the charge-master is most frequently updated from the prior period charge levels based upon some financial analysis determining how much more revenue is required to meet the institution’s revenue targets. This analysis reflects an adjustment for contractuals and the mix of business between key categories of payers. Any major change in payment levels or mix of payers (e.g., Medicaid) requires an adjustment in overall charge-master levels to preserve the required revenue base. Unless there is a major change in how the service items are constructed, the update from one year to the next is fairly straightforward. A recent client project was much more complex as the health system was converting to an integrated charge-master compatible with its new electronic medical record. This required considerable changes in charge-master categories and codes including the mapping of former categories into the new categories.

This process of building the charge-master in this way has resulted in net to gross revenue ratios much less than 40% – 50%, many times as low as 20%. The standard charges are much more than is actually paid. If a price tag was attached to each service as in the retail industry, everything is on sale without people knowing what the sales price is. No other industry has comparable ratios or standard discounts. In most industries, you pay the price on the tag, perhaps with a discount for the sale or closeout pricing.

Pricing Assumptions

Unlike the regulations and limitations affecting health plans in establishing their premium rates, there are no regulatory restrictions affecting how a hospital or health system builds or updates their charge-master. There are no regulations or limitations on the maximum margin built into the pricing. There are no definitions as to what is reasonable.

Medicare, and in some states Medicaid, has some restrictions in terms of what they will consider as an acceptable charge level for services. This is analyzed as part of the Medicare cost reports that hospitals and health systems must complete and file on a regular basis. Commercial payers usually limit their payments to hospitals and health systems based upon negotiated provider contracts. Neither of these approaches (i.e., Medicare cost reports or contractual negotiations) limit or restrict the margin built into the charge-master or resulting net payment.

Reasonable Assumptions

The author is not aware of any restriction or definition of what is a reasonable assumption to be used in building a charge-master or setting individual prices on the charge-master. How much margin is reasonable? When is a charge too large? What responsibility does a hospital or health system have to establish reasonable charges on their charge-master? Is it the responsibility of the health plan or payer to limit these charges to a reasonable level? Would it be better for society if gross billed charges were set at a lesser level, closer to what is actually reimbursed?

Perhaps a more specific example would provide some useful background information. In establishing charge-master prices for supplies or drugs, how much mark-up is reasonable? What factors should be considered in determining that mark-up? In a recent client assignment, the proposed mark-up for supplies was in excess of 500% of the price of the individual supplies, and for lower priced supplies the mark-up was greater than 1000% of the price of the individual supply item. Similar margins were also proposed for pharmaceuticals. What level of mark-up is reasonable? When does it become too much?

I find the use of a continuum helpful in answering these types of questions. At one end of the continuum is financial self-interest. At the other end we have greed. I refer to the G-line as the point where we have moved from financial self-interest to greed. Financial self-interest is not bad or inappropriate behavior. This is where a hospital or health system is trying to be sure they are covering the cost of doing business or the cost of goods, while making a reasonable margin. As charges transition past the G-line, they might be considered egregious, this is a much different situation. I am sure most will agree that at some point along this continuum that the charge is unacceptable or inappropriate. Where is that point? With the fragmented oversight of providers and their charges, the extremely diluted charge awareness of the individual patient, the potential for excessive charges exists.

Learnings from Health Plan Oversight

Concerns about the portion of the premium going towards benefits versus carrier overhead and profit led to minimum loss ratio requirements and oversight. Insurance departments provided a convenient oversight vantage point and process to be sure the consumer was protected from pricing abuse. As this oversight matured the rules were modified to meet the market needs with PPACA providing the latest controls and oversight. These processes recognized the potential for unhealthy behavior by the health plans.

Hospital and health system claims comprise a major component of the health care cost used to calculate the health plan’s loss ratio, yet there is no known oversight of how those health care costs are developed or established. The question is whether or not some level of responsibility and accountability needs to be defined for the hospital and health system providers. How do we protect the health system from unhealthy behavior of health care providers?

AHP Accountability IndexTM (AAI) and Hospital and Health System Pricing

Although pricing issues naturally affect the cost of patient care more than the other two Triple AIM issues (quality of care and health of the population), they do have some residual effect on all of these issues. The following chart summarizes the author’s assessment of AAI for hospital and health system pricing for each of the Triple Aim issues.

| Triple Aim Category | Weight | Rating |

| Patient Experience | 0.333 | 37.5% |

| Population Health | 0.333 | 37.5% |

| Cost of Care | 0.334 | 12.5% |

| Overall | 1.000 | 29.2% |

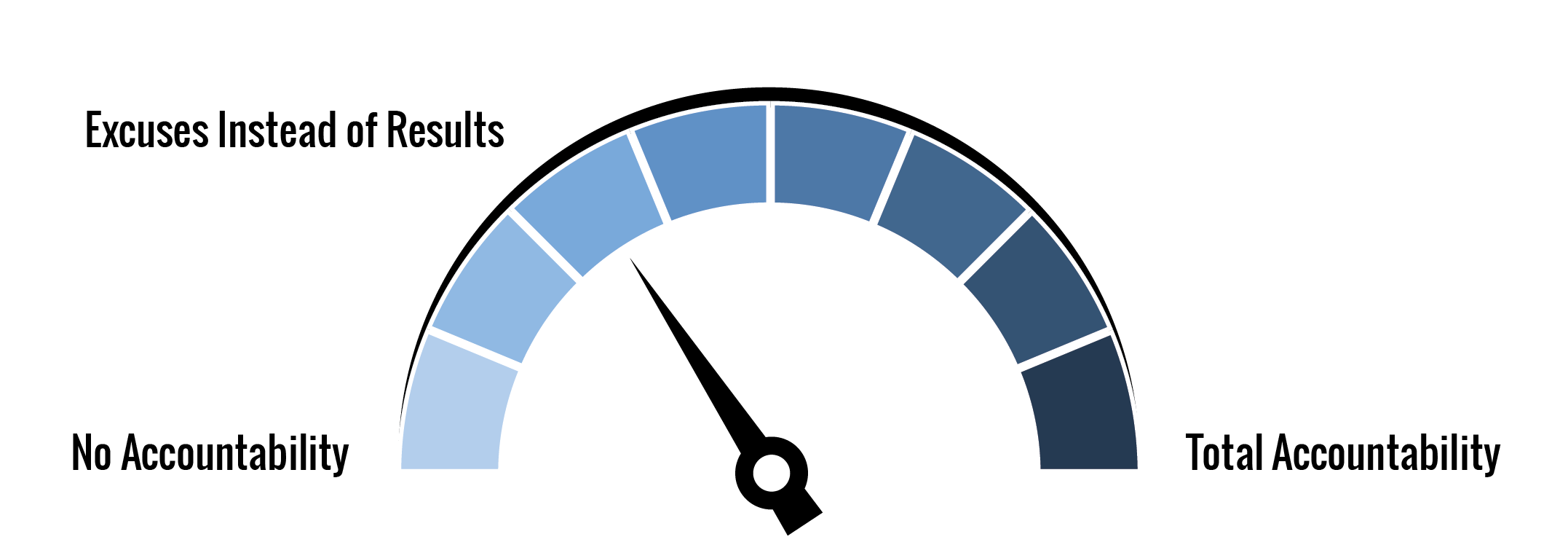

The first two categories have been rated at level 3 of the Accountability Ladder (i.e., Excuses instead of results). This is demonstrated by providers justifying their way out of the question. The higher prices even though diluted through the health system negatively impact the patient experience (i.e., impacting patient satisfaction) and population health. Many patients will not seek the care they need because they can’t afford the care as a result of the high prices. The third category was rated at level 1 since there appears to be no accountability or very limited accountability.

Impact of Improvements in Accountability/Responsibility

Accountability and responsibility can be increased in the health care system through a variety of mechanisms that could readily be implemented. Increasing the transparency of prices in the system is one indirect approach, but assumes that stakeholders will be able to make valid comparisons and take appropriate action. The cost of care, as measured by premium rates, will reduce if inappropriate margins and mark-ups are eliminated or minimized. Providing stakeholders a valid comparison methodology or standard will probably help the process more than anything else.

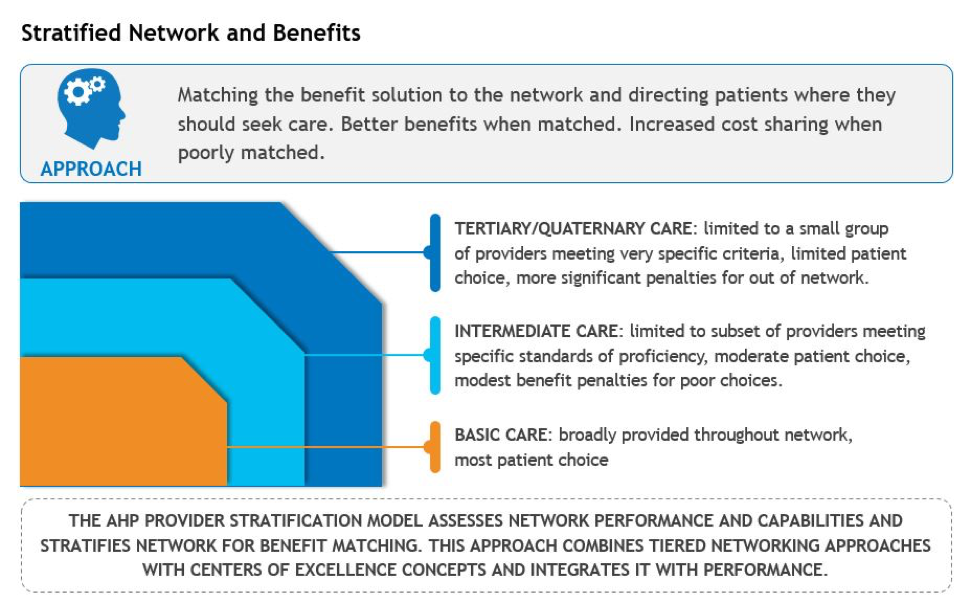

One such methodology that has been used involves the stratification of hospital and health system care into three standardized categories. One approach is shown in the following chart.

Each of these categories of care can be readily defined by MS-DRG for inpatient services. Similar definitions can be developed for outpatient care also. In the example of Basic Care, this level of care is provided by all hospitals no matter how big or small, whether community or academic medical centers. However, the price for Basic Care should be compared across all hospitals with a norm developed for what this type of care should cost. If the same care, obviously meeting appropriate quality and outcome standards can be provided for $X, then comparable care at a higher price suggests unreasonable or inappropriate pricing or an inappropriate setting. For example, if a community hospital is able to provide a specific service for $10,000, then that might be the maximum price any facility should be paid to perform that service. If it costs much more at an alternate facility, then that facility could be deleted from the network or payment to that facility would be limited to the $10,000. This type of pricing constraint would clearly raise the AAI to a much higher level than exists today. For the higher levels of complexity (e.g., Tertiary/Quaternary care), the potential providers would likely be limited to a narrow set of providers where quality outcomes could be assured. The same type of approach could be implemented for Intermediate Care.

This is one approach to implementing more intense accountability into the health system and can be used to increase the AAI to more desirable levels. Such action would significantly improve the results from a Triple Aim perspective also.

Summary Conclusions

There is limited accountability for reasonable pricing in the current health care system. Unfortunately, this has raised the cost of care without appropriate oversight. Much more can be done to improve this without onerous regulations. One aspect of improving our current health care system is the introduction of more intense accountability into the pricing of health care services by hospitals and health systems.

1https://www.oshpd.ca.gov/chargemaster/default.aspx

About the Author

David Axene, FSA, FCA, CERA, MAAA, is the President and Founding Partner of Axene Health Partners, LLC and is based in AHP’s Murrieta, CA office.