Any views or opinions presented in this article are solely those of the author and do not necessarily represent those of the company. AHP accepts no liability for the content of this article, or for the consequences of any actions taken on the basis of the information provided unless that information is subsequently confirmed in writing.

Recognized as a firm deeply engaged in the regulatory and technical aspects of the Patient Protection and Affordable Care Act (ACA), we were invited to provide comments and influence President Obama’s final regulatory enhancements related to his signature domestic achievement. The proposed rule “Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters for 2018” (payment notice) was published in the Federal Register by the Department of Health and Human Services (HHS) on September 6, 2016. This annual update of technical changes is on an earlier schedule than prior cycles with the obvious intention of finalizing rules this year before a new administration takes control.

The payment notice offers many new proposals and is much more than an annual update of benefit and payment parameters for the individual and small group markets. It is widely recognized throughout the industry that substantial changes are required, and a large part of the discussion (294 pages in total) highlights ongoing concerns expressed by stakeholders. Many of the substantive proposals are intended to improve the future of the risk adjustment program. Some stakeholders, including carriers who have exited markets and others who have become insolvent, have characterized these proposals as “too little, too late.” The proposals related to risk adjustment principally address concerns that have been voiced since program inception, although the magnitude of the risk adjustment results have still surprised health plans and state regulators alike.

In addition to risk adjustment enhancements, the other major goal of these proposals is improving the risk pool and enrollment growth in the individual market. Unfortunately, the proposals ignore the real problems and are limited to enforcing special enrollment rules and continuing existing “outreach” efforts.

Our recommendations provided to HHS and summarized here, are in accordance with the inherent purposes of risk adjustment and the desire to create sustainable markets that attract a cross section of eligible enrollees. We also believe it is necessary to build a marketplace that allows insurers that offer efficient, quality coverage to participate without unnecessary volatility or disadvantages. This article discusses the current issues and concerns, the proposals related to risk adjustment, our recommendations, and potential first steps to address the serious problems in the individual market. We should note that our recommendations to HHS were conceptual and based on our experience and our understanding of the proposals. The short (30 day) comment period and lack of detailed data, methods and assumptions accompanying the proposals did not allow a complete actuarial analysis.

Risk Adjustment: Overview

The ACA expands access to health insurance by prohibiting insurers in the individual and small group markets from using health status as an eligibility criteria or as a rating variable. As insurers are not able to select or appropriately rate for the risks they accept, a risk adjustment mechanism is included to appropriately compensate insurers for the risks they enroll.

This ideal is intended to have insurers compete on their ability to provide quality affordable care and an efficient administrative system, while neutralizing the impact of competition based on enrollee selection. A well-constructed program will foster market stability and predictable results. While largely untested in the commercial market prior to the ACA, risk adjustment programs have existed in Medicare Advantage and various state Medicaid programs for many years.

The risk adjustment program applied to ACA markets, intended to stabilize the new marketplaces, has produced surprising (and arguably inequitable and destabilizing) results for many stakeholders, some of which have been legally challenged. The Centers for Medicare and Medicaid Services (CMS), the HHS agency responsible for the risk adjustment methodology, signaled recognition of the concerns well before the payment notice release. In March 2016, CMS released a White Paper1 and facilitated an industry conference to discuss the ongoing concerns. Many of the proposals in the payment notice related to risk adjustment were introduced in the White Paper.

The risk adjustment methodology developed by CMS can be thought of as a two-step process. First, each enrollee in the marketplaces is assigned a risk score based on demographics, benefit plan, and any identified high cost health conditions. Second, to account for risk characteristics that cannot be differentiated by premium rates under the market rules, a “transfer payment” methodology is developed to transfer money from insurers that enroll lower risk enrollees to insurers that enroll higher risk enrollees. CMS designed this methodology to be budget neutral; therefore, all transfer payments are offset by transfer receipts. These two phases are discussed separately.

Risk Adjustment: Risk Assessment

As insurers are not able to select risks or set prices based on the risks received, they must rely on the CMS methodology for an appropriate and adequate financial accommodation. It is therefore imperative that the operational methodology is precise and impartial. The risk adjustment process should accurately assess risk based on health status and related predicted claim costs, and not be influenced by other factors. A risk assessment model requires both appropriate data and appropriate methodology to properly function.

Data Source

The historical data used to calibrate a model should be reflective of the expected population. The current MarketScan® commercial database utilizes data that is not representative of the expected populations. Individuals in this experience base did not have a large concentration of short enrollment durations that are found in the marketplaces. Additionally, medical diagnoses that would result in higher risk scores are less present in the MarketScan® data as insurer revenue was not dependent on this data. For benefit year 2019, HHS proposes to use actual 2016 marketplace data. We have had concerns that the MarketScan® data is not an appropriate approximation of the individual and small group marketplaces; we are therefore in agreement with HHS proposals that move to models based on marketplace experience.

HCC Scoring

Hierarchical Condition Categories (HCC) are used to assign a quantitative health cost risk to each enrollee. The current risk adjustment model overstates the risk/cost for individuals with at least one HCC. As the model is developed to be budget neutral, this necessarily understates the risk/cost of individuals without any HCCs. The HCC bias prohibits the model from achieving the goal of eliminating competition based on enrollee health status. This effectively punishes efficient insurers or those who attract health conscious consumers.

The risk adjustment methodology fails to recognize measurable performance differences as it relates to care management. In our day to day interaction with health plans, we note significant differences in unnecessary utilization of medical services. We have developed an appropriate measure of utilization which we call a Care Management Effectiveness IndexTM (CME Index). In this evaluation approach, the CME Index ranges from 0% to 100%. A 0% CME score describes an extremely ineffective care management process. A 100% CME score describes a high performing care management process with little or no room for improvement. A higher CME Index is related to lower health care costs.

An efficient health plan with a favorable CME Index might be inappropriately associated with lower risk due to quality care management. For example, a plan with a high CME Index might effectively prevent more individuals with diabetes from developing complications which would yield HCC diagnoses. The ACA risk adjustment process will not recognize this occurrence. In fact, HHS directly suggests that low premium plans are “likely underpriced” and unaware of their lower risk population. We disagreed with this general assessment as we often see wide variances in utilization and claim costs unrelated to risk, and we advocated that HHS appropriately recognize the impact of care management.

HHS offers potential remedies for the overcompensation of HCCs, including implementing a complicated “constrained regression” approach that is not explained in detail. This proposal will likely under-predict young enrollees without HCCs. We recommended a simpler, fairer, straight-forward approach that replaces the biased scores with appropriate coefficients. The former CMS Chief Actuary Richard Foster had previously outlined such a solution.

Related to the HCC scoring, we encouraged HHS to explore the impact of the risk adjustment methodology on premium rates (or lack of future offerings) for Bronze plans. We also encouraged HHS to utilize marketplace data to evaluate the reasonableness of the adjustment factors based on metal level.

Partial Year Enrollment

The current methodology does not address the impact of partial year enrollment. In the marketplaces, there are a larger portion of enrollees that are in the market for a short period of time. Unlike the Medicare Advantage program, diagnoses are not tracked by a centralized source so enrollees that change health plans are subsequently counted as not having any HCCs. As claims are episodic in nature, this is problematic for two reasons:

1. When an enrollee is enrolled for only part of the year, a diagnosis related

to higher health care costs may be missed.

2. Even if the diagnosis is captured, the risk adjustment model assumes a full

year of enrollment and accordingly transfers an inadequate amount.

Using a simplified example to illustrate each of these issues, an individual

has a medical condition that will cost $12,000 in December that is diagnosed in October. If the risk adjustment methodology provided $1,000 each month, an insurer that enrolled the individual for the full year would receive $1,000 each month, or $12,000, which would offset the higher cost for this individual. An insurer that enrolled the individual in October would only receive $3,000 and still be responsible for the $12,000 claim. An insurer that enrolled the individual in November would receive no risk adjustment benefit as the condition would not be diagnosed but the insurer would still be responsible for the $12,000 claim.

HHS recognizes this inequity for insurers that have a larger volume of short duration enrollees, which are generally new or growing carriers. HHS has proposed durational factors to increase risk scores of short duration periods.

We believe that this is an appropriate step in the right direction. We did not measure the adequacy of the proposed factors, but noted that the factors for months one to five are less adequate that factors that have been applied historically and generally accepted in the Massachusetts risk adjustment model.

Prescription Drug Claims

There are many benefits to incorporating prescription drug claims in risk adjustment methodology. Pharmacy data are readily available and complete very quickly. They can identify enrollees with HCCs when diagnoses are not coded and also determine severity. Pharmacy data are fairly uniform across the industry and do not have many of the erroneous issues associated with diagnosis data. Inclusion of prescription drug data also results in quicker recognition of high cost conditions and facilitates a more even playing field for new insurers who don’t have medical histories and insurers who are less experienced and less aggressive with financially driven diagnosis coding techniques.

HHS has been reluctant to use pharmacy data due to gaming concerns. We are surprised that HHS appears to be more concerned with pharmacy gaming than the ongoing subjective process of establishing diagnoses, as prescription drug claims cannot be altered after the fact by third parties. HHS intends to cautiously introduce the use of pharmacy data in 2018 with a limited selection of drugs.

We are concerned that this selection may overcompensate the predicted costs for the highest cost enrollees (similar to HCC concern), and therefore undercompensate the predicted costs for other enrollees. Overall, we believe that the stated concerns regarding the use of prescription drug data are exaggerated and we strongly encouraged HHS to appropriately recognize the clear advantages of using prescription drug data. This will not only provide a more accurate risk assessment system, but will facilitate a more level playing field and create a better environment to attract insurers to the marketplaces.

Risk Adjustment: Transfer Formula

The purpose of the transfer formula is to transfer appropriate amounts based on risk. Even with a perfect model of risk assessment, a biased formula will have equity problems. The applied methodology uses a Statewide Average Premium (SWAP) to calculate transfer amounts and results in imbalanced transfers that harms low cost and efficient insurers. The formula transfers significant sums of money based on items that are not predictable and not based on actuarial risk.

The “statewide” nature of the formula is problematic. Regional practices are different and coding patterns are often higher in major metropolitan areas which causes risk transfer payments to be based on regional physician practice patterns rather than health status or actuarial risk.

The “average” nature of the formula severely exaggerates risk transfers for efficient insurers by mandating an inflated transfer amount relative to their cost structure. This particularly impacts small insurers who experience the most unpredictability and volatility with risk adjustment results.

The “premium” nature of the formula is not appropriate. The calculation penalizes efficient insurers with the inclusion of administrative costs in the formula. As transfer payments are based on premium amounts rather than claims, low cost insurers pay an inflated amount based upon reasons unrelated to claims risk. Many other risk adjustment methodologies, including Medicare Advantage, appropriately recognize only the claims portion of the costs.

Low cost insurers often offer plan options that attract the type of individuals that improve the overall risk pool, yet they are penalized by the methodology which necessitates price increases. This unintended consequence may limit insurers’ ability to attract low cost enrollees.

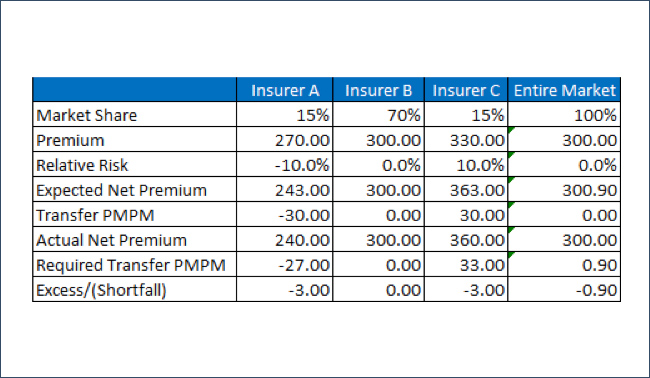

To illustrate these dynamics, we begin with an American Academy of Actuaries Subcommittee example and change some variables to demonstrate the formula impact. The table below shows the impact of using a SWAP rather than an insurer’s own premium. From the perspective of Insurer A, a premium PMPM of $270 and a relative risk of -10% should result in a risk adjusted premium of $270 * (1 – 10%) = $243. Since the SWAP is $300, the Insurer A transfer payment is $30 ($300 * 10%) and the risk adjusted premium is $240, resulting in a $3 inadequacy.

The pricing obligations of the ACA risk adjustment methodology require insurers to base rates on the market profile rather that their own population. For small insurers, this is a monumental challenge as they are not privy to other insurers’ enrollment data. The next few tables illustrate the elements that could cause the risk adjustment results to change, each of which are not relevant the risk of an insurer’s population nor reasonable to project in the pricing process.

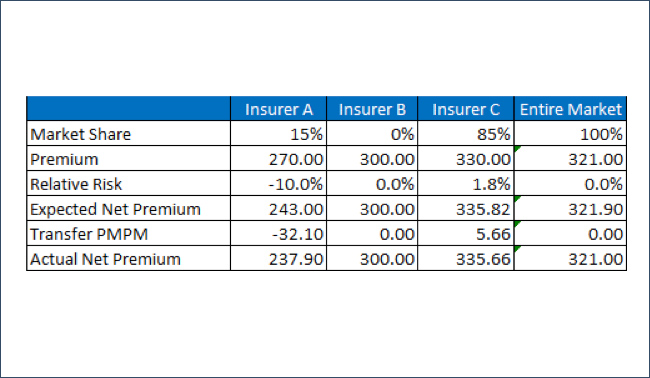

Maintaining the perspective of Insurer A, consider the scenario where Insurer B exits the market and all of Insurer B’s members enroll with Insurer C. Insurer A’s population does not change but the SWAP is increased as members move to a higher cost insurer. Insurer A’s PMPM risk adjustment transfer assessment increases from $30.00 to $32.10 with no changes in the risk pool, simply due to differing enrollment decisions amongst other insurers; note that this concept is also true if Insurer C remained in the marketplace and there was simply migration of members from Insurer B to Insurer C or vice versa.

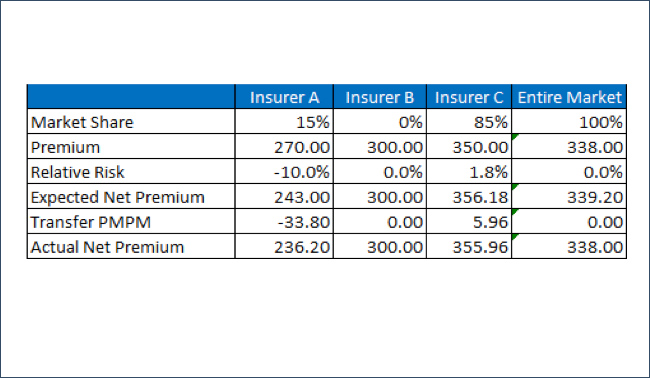

Now consider if Insurer C has a premium rate of $350 rather than $330. As the SWAP is increased, Insurer A’s PMPM risk adjustment transfer assessment increases from $32.10 to $33.80. There has been no change in the risk population of either Insurer A or Insurer C, yet both have different risk adjustment transfer settlement solely due to the premium change for Insurer C. It is also troubling that Insurer C could increase its risk adjustment payment simply by increasing its premium rate.

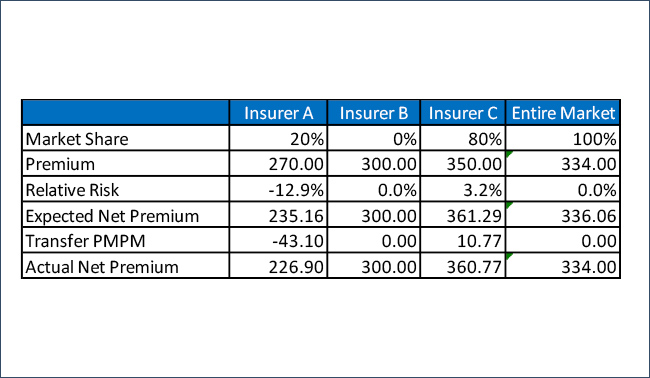

The final illustration hypothesizes the first change in the risk pool. Assume that Insurer’s C 85% market share is made up of 60% of the market with a relative risk of 6.7% and 25% of the market with a relative risk of -10.0%. Due to the high rates, the 25% with a relative risk of -10% exits the marketplace. Insurer A has a larger market share in the reduced market. As enrollees with a low relative risk left the market, Insurer A’s relative risk profile is now lower even though its enrolled population did not change. The PMPM transfer is now $43.10 due to change in enrollment in the overall market.

With the current influx in the markets, these examples illustrating insurer exits and enrollee migration between plans and on/off the marketplaces are very real and yet unpredictable. Unfortunately, the risk adjustment methodology applied by HHS has introduced many more variables to the transfer formula that are not related to claims risk and unreasonable for pricing actuaries to project.

Risk Adjustment: Unpredictability

The unpredictability of risk adjustment transfer amounts continues to put upward pressure on premiums. The timing of risk adjustment determinations relative to premium submission due dates continues to be problematic. The lack of health plan stability in markets and transfers of membership exacerbates the

unpredictable nature of risk adjustment transfer payments.

Many insurers have exited the market, have contemplated such a decision, or have become insolvent due to financial results and predictability concerns. The risk adjustment results have often been cited as the “surprise” financial item in poor results. The marketplaces initially attracted new health plans which have been subject to alarming transfer amounts that represent a significant portion of their premium. We believe that many of the program dynamics responsible for the unpredictability are not adequately addressed in the proposed rule.

As it exists today, the unpredictability of the methodology is arguably having a destabilizing impact. As a consulting firm that explains actuarial concepts to stakeholders, we have encountered situations with health plans who are so disillusioned by these results that we cannot even begin a general conversation about the methodology mechanics. State regulators have also struggled with comprehension as they have managed many new solvency concerns that caught them by surprise. The state of New York released an emergency regulation to reverse “stabilize” the ACA impact in the small group market. We advocated that it would be best for HHS to proactively address instability and avoid potentially inconsistent and/or inadequate state-based adjustments.

The use of a SWAP adds to the predictability challenges and creates an untenable situation for insurers that do not command a large market share. Due to their size, large insurers strongly influence both the average premium and risk score. They have a large contribution to both the average risk score and the SWAP which results in less volatile consequences. Notably, even some large insurers have been surprised by the formula results. The inequities and volatility created by usage of a SWAP need to be addressed for the markets to succeed.

Risk Adjustment: Pricing Implications

As mentioned above, insurers have historically based rates on their own risk profile. A risk adjustment methodology should allow an insurer to change from pricing a specific risk to an average risk and rely on risk adjustment payments to bridge only that difference. The HHS risk adjustment methodology introduces many other variables and creates unreasonable predictability expectations. Even with an accurate and impartial risk scoring methodology, insurers would need to be able to project a considerable amount of extraneous variables to fully and appropriately consider risk adjustment transfers in pricing formulas. To accurately project actual revenue, the pricing actuary needs to estimate each of the following which currently influence risk adjustment transfer payments:

1. Risk profile of eligible enrollees

2. Risk profile of who enrolls in market versus who does not enroll

3. Insurer’s relative risk to the market

4. Premium rates of all other insurers

5. Enrollment by benefit plan and region of all insurers

6. Health status of each insurer

7. Coding efficiency of each insurer

Risk Adjustment: Final Thoughts

Successful risk adjustment models foster predictability and eliminate incentives for enrollee selection based on specific health conditions. They equitably adjust premium levels to reflect the health status or actuarial risk of an enrolled population. They provide impartial treatment for all health plans, and do not offer advantages based on size, growth patterns, breadth of network, efficiencies, medical management, or cost structure. The current risk adjustment results are altered by including multiple variables unrelated to claim cost risks. The current methodology systematically harms cost effective insurers, and the penalty is magnified for smaller insurers. The methodology further inflates the damages by including administrative expenses in the formula.

As it exists today, the risk adjustment methodology is preferential to existing health plans who enroll high risk individuals and charge high premiums. The exclusion of prescription drug claims and the lack of recognition for partial year enrollees further misestimates the relative actuarial risk between new and existing insurers. These imbalanced assessments penalize the type of insurers and enrollees that the ACA seeks to attract.

Individual Market Sustainability

The individual market is more fragile due to the underlying incentives for prospective enrollees that are present in the net premium calculations. This fragility adds to the instability in the individual market and creates an even more challenging and unpredictable risk adjustment environment.

It was recognized from the beginning of the program that adequate participation from young and healthy individuals is required for success, so targeted promotional efforts and outreach have focused on a younger demographic. These efforts continue as young adults are offered the lowest value proposition and remain the eligible demographic with the highest uninsured rates. The dynamics of the rating rules and the premium subsidy allocation2 are attracting a skewed enrollment mix and creating significant financial challenges for health plans. The underlying mechanics of the subsidy provisions continue to produce results that make the program relatively unattractive to younger enrollees. Older adults actually pay less than young adults at the same income level for the same coverage for some plans. The propose rule does not offer any solutions for these unintended consequences.

Risk Adjustment Impact

As discussed, the risk adjustment methodology requires the pricing actuary to predict many things that are outside the scope of traditional pricing mechanics and unrelated to the risk profile of the insurer population or the market population. The current individual marketplace is unattractive to insurers and young healthy individuals alike. Accordingly, there is significant turmoil in the market with insurers leaving, individuals staying for a short time, and individuals changing insurers. This market volatility adds to the unpredictability of the risk adjustment calculations and magnifies the existing concerns.

We advised HHS that the enrollment of varying health risks cannot be solved by the risk adjustment process alone. An application of the current risk adjustment methodology only allows HHS to transfer money between insurers; is does not compensate for a higher than average risk market enrollment. It is important to achieve a stabilized risk pool to allows insurers to understand the ongoing health status of the overall market as well as the relative risks of their own populations.

Real Solutions

We recognize that all of the enrollment challenges related to the underlying enrollee incentives cannot be resolved through federal regulations. From an administrative standpoint, HHS should work proactively with states and interested stakeholders to facilitate State Innovation Waivers3 under Section 1332 that allow states to use existing federal funds to create a broader market appeal. This is a more constructive use of time and resources than merely continuing the outreach efforts to introduce the new markets. We encouraged HHS to explore real solutions and not to expend fees intended for exchange operations to expand such outreach.

Summary

As private and public partners with many stakeholders in the health care arena, we are committed to developing sustainable health care markets that offer solutions to health plans, health care consumers, regulators, and policymakers. We were honored to be asked to contribute to the enhancement of these important regulations. Our recommendations are intended to strengthen and stabilize markets, and create incentives that attract a cross section of eligible enrollees across the age/income spectrum. These recommendations are in line with the policy goals of promoting innovation and fostering competition. We look forward to the implementation of these enhancements, which will improve predictability for health plans and facilitate more robust, stable marketplaces.

1 https://www.cms.gov/CCIIO/Resources/Forms-Reports-and-Other-Resources/Downloads/RA-March-31-White-Paper-032416.pdf

2 “Implications of Individual Subsidies in the Affordable Care Act—What Stakeholders Need to Understand,”

https://soa.org/news-and-ublications/newsletters/health/pub-health-section-newsletters-details.aspx

3 “Section 1332 Waivers. Coming Soon to a State Near You?”

http://healthwatch.soa.org/?issueID=1&pageID=33

About the Author

Greg Fann, FSA, FCA, MAAA, is a Senior Consulting Actuary with Axene Health Partners, LLC and is based in AHP’s Murrieta, CA office.