My father is an immigrant who fled the Civil War in El Salvador during the 1980s and my mother is a descendant of Irish immigrants who arrived in New York searching for a better life. From our founding fathers who risked life and limb to confront the most powerful empire the world had ever known to our immediate fore fathers who left their homelands in pursuit of the American dream, we are a nation unafraid of risking it all for the transcendent desires of the human heart. It should come as no surprise then, that our nation has turned to another revolutionary battle that will forever change our great country. This time, the shot heard round the world will not be literal gunshots the likes of heard in Lexington and Concord but rather political shouts of ‘Medicare for All’ from the likes of Sanders and Warren. But is this revolutionary movement advancing the dreams of our forefathers or is it an attack on our values requiring a counter revolution to preserve our liberty?

The Tipping Point

There comes a moment where a problem that everybody recognizes reaches the point of no return where the status quo is untenable, and a radical solution becomes the only visible way out. In health care, rising costs that are increasingly applying pressure on government expenditures, employer expenses and consumer wealth have given political fuel to the ‘Medicare for All’ movement that seeks a revolutionary change to the system. Before delving into the revolution, it is worth exploring why health care costs are high in the first place.

Many believe that approximately 1/3 of health care spending is “wasteful” or in other words does not contribute to patient health or care quality[1]. With health care spending rising to 18% of the national GDP, this 33% equates to over $1 trillion of annual waste. Yet, the leper in the room that nobody wants to touch is that the main problem with the $1 trillion of “waste” is that…we are already willing to pay it! The ideal price of a commodity is an organic matching of supply and demand that reflects what the consumer is willing to pay and what the producer is willing to accept. Most individual consumers in America have been inorganically shielded from the actual cost of care which in turn has shielded the health care industry from having to focus on consumer value or cost. Government-sponsored insurance covers approximately 41%[2] of the population and pays for roughly 79%[3] of the cost of care. Employer sponsored insurance covers approximately 47%[4] of the population and pays for roughly 48%[5] of the cost of care. Both are funded with consumer dollars but are done so through payroll reductions (i.e., government programs through taxes and employer programs partially through contributions). The result is a system in which health care funding is largely driven by political desires to appeal to voters and staffing desires to appeal to employees as opposed to consumer desires for quality health care.

We all want to reduce health care spending but few like to acknowledge the full scope of employment opportunity and wealth the industry creates and what it would mean to truly lower health care costs in America. As former Princeton economist Uwe Reinhardt puts it, “Every dollar of health care spending is someone else’s health care income. Even when it’s fraud, waste or abuse.”[6] It’s easy to garner support for eliminating fraud, waste and abuse but as the quote points out, doing so would result in eliminating revenue, jobs and income, a much harder sell. Solutions to rising health care costs have naturally focused on the easier sell of efficiency measures but have failed to control costs due to a lack of attention to the harder issue of over funding. In a sense we have put the efficiency cart before the funding horse. In America, efficiency is certainly part of the solution, but lack of efficiency is not the source of the problem.

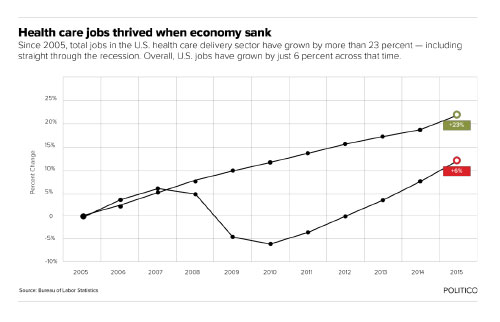

To understand the problem further, we need to first recognize the largest barrier to reducing costs. The following graph shows health care and overall job growth since 2005. The top line is health care job growth, the bottom line is overall job growth (which includes health care jobs).

Bending the health care cost curve means bending that job growth curve as well. When you hear the word “waste”, translate that to “wages and employment” and you will have a better grasp on the issue. Nobody volunteers to reduce their own income or revenue for their company. There is only one way to lower wages or revenue, which is by force. And there are only two forces to leverage, free market competition and government mandate.

As it stands now in America, we have collectively “decided” to put over $3 trillion on the table for the health care industry and they have no incentive to not take it to the bank and ask for more the next year. Other industries are limited by consumer choice and what we are willing to pay. By funding health care through payroll taxes and deductions, the average consumer rarely makes elective decisions on whether to put their money on the table and whether the services they receive are worth the money given.

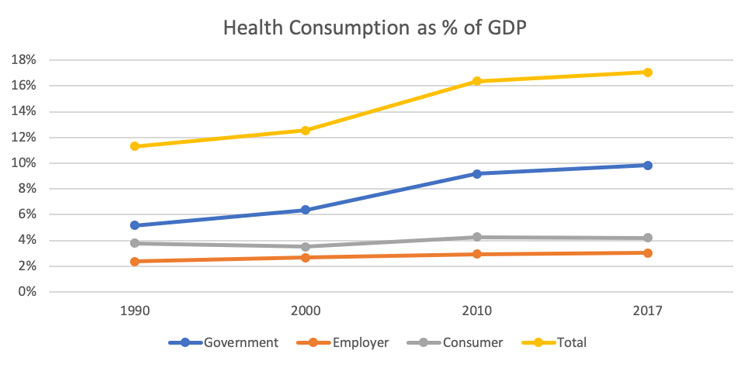

The following graph shows the rise of health care consumption as a percentage of GDP from 1990 to 2017. The employer and consumer portion of health care consumption excludes taxes paid to fund Medicare and Medicaid which is allocated to the Government line. While everything the government does is funded by citizens and employers, the direct impact on how much is spent by the government is severed through taxes. In other words, the graph represents the direct elective costs employers and consumers pay vs the amount spent on and paid towards government programs.

Health care consumption has risen as a percentage of national GDP while consumer out of pocket costs (premiums, cost sharing, uncovered benefits) and employer elective contributions have remained flat. It is impossible to know what the consumer threshold would be if consumers paid all of their health care costs directly out of pocket but it is safe to assume it is somewhere between the current 4% and 17% and likely closer to the 4%. If consumers were 100% responsible for their health care expenditures, you can be 100% sure that health care would be less expensive simply because we would not put as much money on the table.

Reformation or Revolution?

Don’t you know they’re talkin’ about a revolution, it sounds like a whisper

And finally the tables are starting to turn, talkin’ ’bout a revolution

– Tracy Chapman

When encountering large systemic issues such as rising health care costs, there are two types of solutions to consider, solutions that reform and solutions that revolutionize. Reform causes the least amount of disruption and therefore should always be our first option, while revolutions necessitate major disruptions that should be a last resort to be used when reform is impossible.

The political stage has been set for a debate in the upcoming presidential election cycle about a revolutionary solution colloquially known as ‘Medicare for All’ (single-payer system). While the main critiques of the proposals rightfully center on the federal cost of such programs and the dangers of socialism, detractors usually fail to acknowledge that a single-payer system does in fact address the main issue of rising health care costs…over funding. Returning to our two levers, competition and government mandate, single-payer proposals will give the government the ability to control health care costs by controlling how much money enters the system. If you consider that Medicaid and Medicare physician and hospital reimbursements can be as low as 50% of what private insurance companies pay, simply moving the entire health care system to government fee schedules could reduce overall health care costs by up to 40%. It would be a mistake to focus solely on the wide arrange of problems with a single-payer system without also acknowledging that it is a valid, workable option for our country that would leverage government power to reduce health care costs and expand coverage to marginalized individuals.

For the United States, the issue with a single-payer system is not whether it will accomplish a particular end or not, in this case lowering health care costs and expanding coverage. ‘Medicare for All’ may in the end be a success but the same could be said of the People’s Republic of China, the world’s second largest economy. The issue with ‘Medicare for All’ is that it is fundamentallyun-American.Our country was established in order to avoid utilizing the central government lever in favor of a free market system that empowers individuals and preserves economic liberty. On the other hand, the socialist instinct is to cede individual autonomy for the collective good by giving centralized power to intellectual elites who will decide how to order society properly. Underlying the socialist ideology is a benevolent disdain of the common man that seeks to take care of the masses with the assumption that the masses are poorly equipped to take care of themselves.

As a Catholic, the instinct to help the less fortunate is also a commandment of God. I empathize with the impulse driving the public which is not the benevolent disdain of the socialist ideology but rather the genuine desire to reach out to the marginalized, protecting them against a predatory capitalistic society. However, utilizing a socialist political ideology to accomplish this end is a misguided effort that fails to acknowledge what is lost in the process. Taxing Americans, collecting their wealth and centralizing the power of that wealth to control the health care industry also means giving up individual control of your own health care. A single-payer system will undoubtedly mean most Americans will be subject to the values of a few intellectuals influenced by powerful bureaucrats deciding for all of us what (or who?) should or should not be valued. Not to mention the resulting unintended consequences of price controls that will assuredly result in some degree of medical service shortages. Neither my Catholic faith which formally rejects socialism[7] as an intrinsically immoral form of government nor my American heritage teaches me to put that much trust in the hands of a powerful government.

It is important to keep in mind that one side of the political spectrum is starting down a revolutionary path to solve the issue of rising health care costs. The issue itself must be solved. Like it or not, our country has arrived at an impasse in terms of how to reform our health care system and the idea of incremental reform is all but dead. Whether it’s 2020, 2024, 2028 or beyond, a single-payer system will be on the ballot and will eventually succeed unless an equally radical solution tackling the main issue of funding is proposed and successfully articulated to the American people. A counter revolution will necessitate a generation ready to sacrifice and risk it all to preserve the liberty fought for by our founding fathers and pursued by ancestors. Are we courageous enough?

The Counter Revolution

Don’t you know you better run run run…

A counter revolution that runs from the final goal of a single-payer system will need to acknowledge the unique challenges of health care and provide for a path forward. The main purpose of the article is to establish over funding as the primary issue to be solved and to push forward the reality that status quo solutions will be defeated by revolutionary solutions. To give a flavor of what a counter revolutionary response would look like, I have developed high level thoughts to consider in the form of the following interconnected proposals.

There are three principles to guide solutions that correspond to three market distortions unique to health care. The three market distortions are:

- Free services: we do not deny health care services to those who cannot pay but instead pass the cost on to those who can.

- Consumer responsibility: consumers interact with the health care system and can assess value but are shielded from the cost of care by third party funding.

- Outlier health outcomes: a small amount of people contribute to a large amount of costs which requires pooling of funds and specific protections.

From these problems in health care, any viable solution must focus on the following three principles:

- Consumer Purchasing Power

- Consumer Choice

- Consumer Protection

Consumer Purchasing Power

Those who struggle financially to afford quality health care deserve both financial assistances to give them purchasing power and the dignity to make responsible choices. Our current system is a form of wealth redistribution that collects and centralizes the wealth through taxation, then leverages that power to demand price controls (government fee schedules) while “redistributing” benefits back to lower income folks (Medicaid) and the elderly (Medicare). A revolutionary change to this system should maintain wealth redistribution but do so in a way that disperses economic purchasing power as opposed to centralizing it.

- Establish government issued Health Savings Accounts (HSA) at birth.

- Eliminate requirements to purchase HDHP insurance plans and contribution limits for HSA accounts and create accounts at the same moment a social security number is given.

- All HSA contributions will be tax free and can be spent tax free on any health care costs including premiums, out of pocket costs, LTC payments, etc.

- Employers, employees, family members and governments may contribute to HSA accounts.

- Eliminate Medicare and Medicaid by phasing out benefits and phasing in targeted federal HSA distributions and premium subsidies.

- Medicare benefits will remain intact for those currently aged 40 and older. Funding will continue through income taxes but individuals younger than 40 will no longer receive benefits at age 65. (Millennials must be the second greatest generation and sacrifice).

- Tax revenues will be redistributed through HSA distributions and premium subsidies to low income individuals and families making under 400% of the FPL under age 65 and all individuals over age 65.

- Total tax distributions for the new program will target 75% of current Medicare, Medicaid and ACA subsidy spending. This would currently amount to almost $1 trillion. With 60%[8] of the population falling under 400% of FPL, that equates to over $5,000 per person.

Take a breath, breathe, yes I believe we can and should eliminate the golden calf of Medicare. Your health is your responsibility and I believe that people are dignified enough to be trusted with that responsibility. 401k accounts and retirement plans necessitate sacrifice and life planning. Paying for health care in old age should be the same. Health should not be viewed annually but in terms of a life long commitment. HSA accounts that have investment yields and can be contributed to by consumers, employers and governments can be an empowering way to push individuals in America to care about their own health and how its funded.

To some degree Medicare already incorporates this idea through lifelong taxation but is not elective which severs ownership and responsibility. For those who have contributed less than 15 years into the Medicare trust fund, a new program reflecting new values should be implemented. Millennials, more so than any other generation before them, are very attune to their own health and how it will affect their lifestyle in the long run. I believe we are the generation ready for this change in responsibility.

Consumer Choice

A free market solution to health care costs requires the ability for consumers to have options with their spending. When the money is not guaranteed to the health care industry, the response will be a rush to create products and services that are both high quality and cost efficient. Federal assistance as well as health care funding should therefore seek as many possible choices of how consumers can spend their money.

- Equal tax treatment of all LTC or health insurance (premium/cost sharing) spending by making these expenditures tax deductible.

- Premiums and all health care spending tied to an insurance plan will be tax deductible whether spent out of pocket, through employer sponsored insurance or insurance purchased in the open market.

- HSA funds can be used for distributions not directly related to health care.

- Individuals can transfer funds to family members or people they wish to help tax free.

- Cash withdrawals will be taxed at 50% and any funds left over at death will be given to beneficiary’s tax free.

- Eliminate strict federal regulations on health care plans and allow states to fully develop mandates and requirements that suit their populations.

- QHP plans will remain in effect for the distribution of premium subsidies but non-QHPs that give alternative coverage will be allowed on a federal level.

- State governments and DOI’s are free to add regulations and control their markets as they see fit. State’s can also add contributions to the HSA accounts of their residents along with any other state funded systems.

Consumer Protection

Children should be given equal opportunity to establish themselves financially and invest in their future health needs regardless of economic background. Further, people who have a pre-existing condition should be protected from being excluded from the health care system. To counter balance the pre-existing condition protection, responsibility of coverage should be enforced through greater penalties for those who do not remain covered. These penalties will not be government penalties but allowable rating differences and rules for insurance companies accepting certain applicants.

- Keep the current ACA exchange market structure intact but split the market in two: Qualified Health Plans and Non-Qualified Health Plans.

- QHPs will have minimum AV and benefit requirements, rating restrictions and guaranteed issue (pre-existing condition protection) requirements.

- QHPs can be both employer sponsored or bought on the individual market though the federal premium subsidies will only be available in the individual market.

- If minimum coverage is maintained, guarantee issue privileges with no health status rating are maintained. If minimum coverage is not maintained, guarantee issue privileges are maintained but carriers can underwrite the application and charge higher premiums.

- Industry subsidized high risk pool established in the individual market.

- An invisible high risk pool will be established in the individual market where QHP carriers can underwrite and pull out individuals into a separate shared pool of risk.

- All health plans, QHP and non-QHP will pay a percent of premium to fund the high risk pool.

- Federal HSA distributions will be annually made to accounts up to the age of 18 regardless of income.

- Annual federal contributions will be made to all children up to the age of 18.

- These funds can only be used for medical services of that child and cannot be taken by the parents for any other purpose.

The Declaration of Health Care Independence

When in the course of human events it becomes necessary for one people to dissolve the health care funding bands which have connected them with one another…a decent respect to the opinions of mankind requires that they should declare the causes which impel them to the separation.

We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Health Care. — That to secure these rights, Government Programs are instituted among Men, deriving their just powers from the consent of the governed, — That whenever any Form of Government Programs becomes destructive of these ends, it is the Right of the People to alter or to abolish it, and to institute new Government Programs…Prudence, indeed, will dictate that Government Programs long established should not be changed for light and transient causes; But when a long train of abuses and waste, pursuing invariably Medicare for All evinces a design to reduce them under absolute Despotism, it is their right, it is their duty, to throw off such Government Programs— Such has been the patient sufferance of these Health Care Consumers; and such is now the necessity which constrains them to alter their former Systems of Government Health Care. The history of the present Medicare and Medicaid programs is a history of repeated injuries and usurpations, all having in direct object the establishment of an absolute Tyranny of Medicare for All over these States.

— And for the support of this Declaration, with a firm reliance on the protection of Divine Providence, we mutually pledge to each other our Lives, our Fortunes, and our sacred Health.

Let the revolutionary battle begin…

End Notes

[1]https://www.healthaffairs.org/do/10.1377/hblog20180530.245587/full/

[2]The National Health Expenditures Accounts table 22 (Medicare, Medicaid, other public enrollment).

[3]Medicare enrollees pay on average 33% of the total cost of care through premiums and cost sharing and assumed 0% for Medicaid. https://www.kff.org/medicare/issue-brief/an-overview-of-medicare/

[4]The National Health Expenditures Accounts table 22 (Employer-sponsored).

[5]Employees pay on average 34% of the premium (NHE) and assumed 85% average AV for OOP cost sharing.

[6]https://www.politico.com/agenda/story/2016/07/what-is-the-effect-of-obamacare-economy-000164

About the Author

Guest Post – Daniel Cruz, ASA, MAAA

Any views or opinions presented in this article are solely those of the author and do not necessarily represent those of the company. AHP accepts no liability for the content of this article, or for the consequences of any actions taken on the basis of the information provided unless that information is subsequently confirmed in writing.